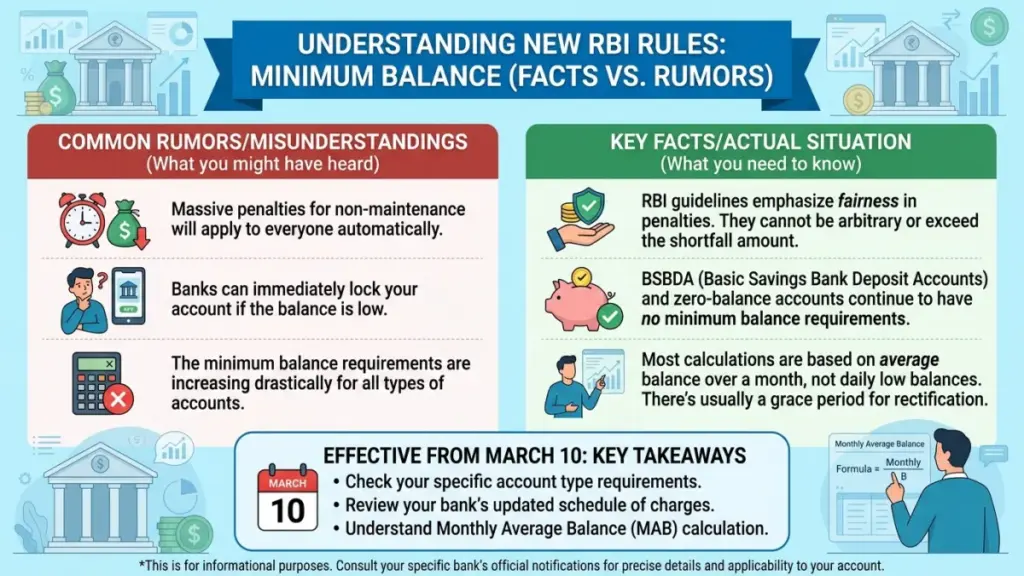

India’s banking customers may soon see clearer rules around minimum balance requirements in savings and current accounts. A revised regulatory framework linked to the Reserve Bank of India’s ongoing efforts to improve transparency in retail banking is expected to take effect from March 10, 2026. The update has drawn attention because minimum balance rules have historically varied widely between banks, and sometimes even between branches of the same institution.

For many account holders, penalties linked to low balance have often appeared without clear understanding of how the requirement was calculated. According to reports, the new approach seeks to simplify these expectations by establishing broader reference benchmarks across metro, urban, semi-urban and rural locations. The intention is not to impose a single rigid rule but to create clearer guidelines that banks can follow while still offering different account types.

The timing of the revision is notable as digital banking usage continues to expand across the country. Millions of customers now operate accounts through mobile apps, digital wallets and automated payments, making consistent balance rules increasingly relevant. While the updated framework may bring more clarity, final implementation details such as penalty structures, grace periods and product features will still depend on individual banks.

Standardised Balance Benchmarks for Different Regions

Based on available information, savings account holders in metro and urban areas may be expected to maintain an average monthly balance of around ₹3,000. In semi-urban and rural branches, the indicative requirement may be approximately ₹1,500. The differentiation reflects variations in income levels and cost of living across regions while attempting to bring greater uniformity to the overall banking structure.

Current accounts, typically used by traders, businesses and professionals with higher transaction volumes, may continue to have higher balance requirements. However, the revised framework aims to narrow the wide differences that previously existed between institutions. In practical terms, customers may find it easier to anticipate balance expectations when opening accounts in different cities or transferring accounts between branches.

Digital Banking Growth Driving Regulatory Adjustments

India’s banking ecosystem has evolved rapidly over the past decade. Digital payment platforms, mobile banking apps and Unified Payments Interface transactions have reshaped how individuals manage money. Despite this shift, many minimum balance policies were still designed around branch-centric operations, creating confusion for customers who frequently move or maintain multiple accounts.

A banking analyst familiar with retail finance trends noted that greater standardisation is “a logical step in a system where customers interact with banks primarily through digital platforms rather than physical branches.” According to this perspective, clearer benchmarks may help reduce disputes related to unexpected deductions, especially when customers relocate or shift accounts between urban and semi-urban areas.

Possible Effects on Salaried Workers, Students and Small Traders

For salaried professionals receiving regular monthly deposits, maintaining a few thousand rupees as an average balance may not create major financial strain. However, individuals with irregular income patterns could experience the impact more directly. Students, freelancers, pensioners and small traders sometimes operate with fluctuating balances depending on expenses and payment cycles.

Consider a freelance designer who receives project payments at irregular intervals while managing several automated subscriptions and digital payments. If multiple debits occur early in the month and the balance remains low for several days, the average monthly balance could fall below the required level even if funds are later deposited. Under bank rules, this situation may trigger penalty charges depending on the institution’s policies.

How the New Framework Differs from Earlier Banking Practices

In earlier years, public sector banks generally kept minimum balance requirements relatively modest, while some private banks applied higher thresholds, particularly in metropolitan branches. Penalty structures also differed widely. Some banks charged fixed fees while others calculated penalties based on the percentage shortfall from the required balance.

The new framework signals a shift toward more customer-focused regulation. Supporters argue that clearer benchmarks may reduce confusion and help customers compare banking products more easily. Critics, however, point out that banks may lose some flexibility in designing differentiated account packages. The long-term outcome will likely depend on how individual banks adapt their offerings once the updated guidelines take effect.

Average Monthly Balance: A Frequently Misunderstood Calculation

One of the most common misunderstandings among account holders involves how minimum balance requirements are calculated. In most cases, banks measure the average monthly balance rather than checking the closing balance on the last day of the month. This average is usually calculated by adding daily end-of-day balances and dividing the total by the number of days in the month.

For example, an account that holds ₹6,000 for the first ten days but drops to ₹500 for the remaining twenty days may still fall below the required average balance. In practical terms, maintaining higher funds early in the month does not necessarily offset prolonged low balances later. Understanding this calculation method may help customers avoid avoidable penalty charges.

Notification Systems and Basic Savings Account Alternatives

Many banks have started improving real-time alerts through SMS and mobile banking apps. These alerts notify customers when account balances approach or fall below the minimum threshold. According to available documents, such notification systems are intended to give account holders time to add funds before penalties are applied.

Another option gaining attention is the basic savings bank account, which generally does not require a minimum balance. These accounts are often linked to financial inclusion initiatives and provide essential banking services. However, they may include restrictions on the number of free transactions or certain service features. Customers exploring these options should review the specific terms offered by their bank.

Steps Customers May Consider Before the Implementation Date

With the revised framework expected to come into effect in March 2026, banks are likely to communicate updated requirements through official notifications, SMS alerts and mobile app messages. Customers managing several accounts may consider reviewing dormant or rarely used accounts to ensure they are not unintentionally incurring charges.

In practical terms, checking recent account statements, enabling low-balance alerts and reviewing automatic payment instructions may help maintain the required average balance. Verification is recommended before making changes based solely on news updates, as detailed rules and exemptions may differ between banks and account categories.

Disclaimer: This article is based on publicly available information and emerging updates regarding banking regulations. Minimum balance requirements, penalties and exemptions may vary depending on the bank, account category and official notifications. Readers are advised to confirm details through their bank’s official website, customer support channels or branch representatives before making financial decisions.